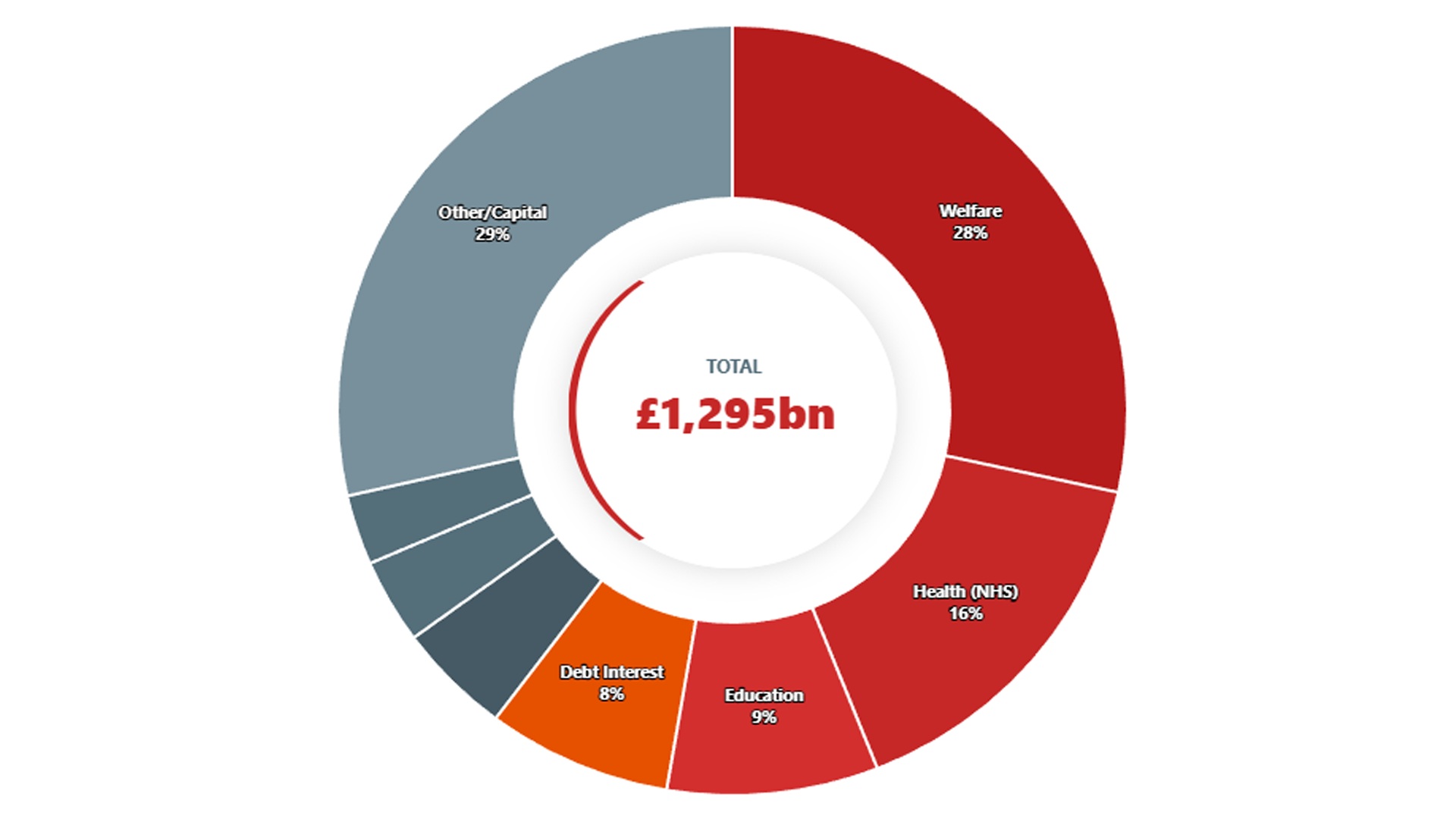

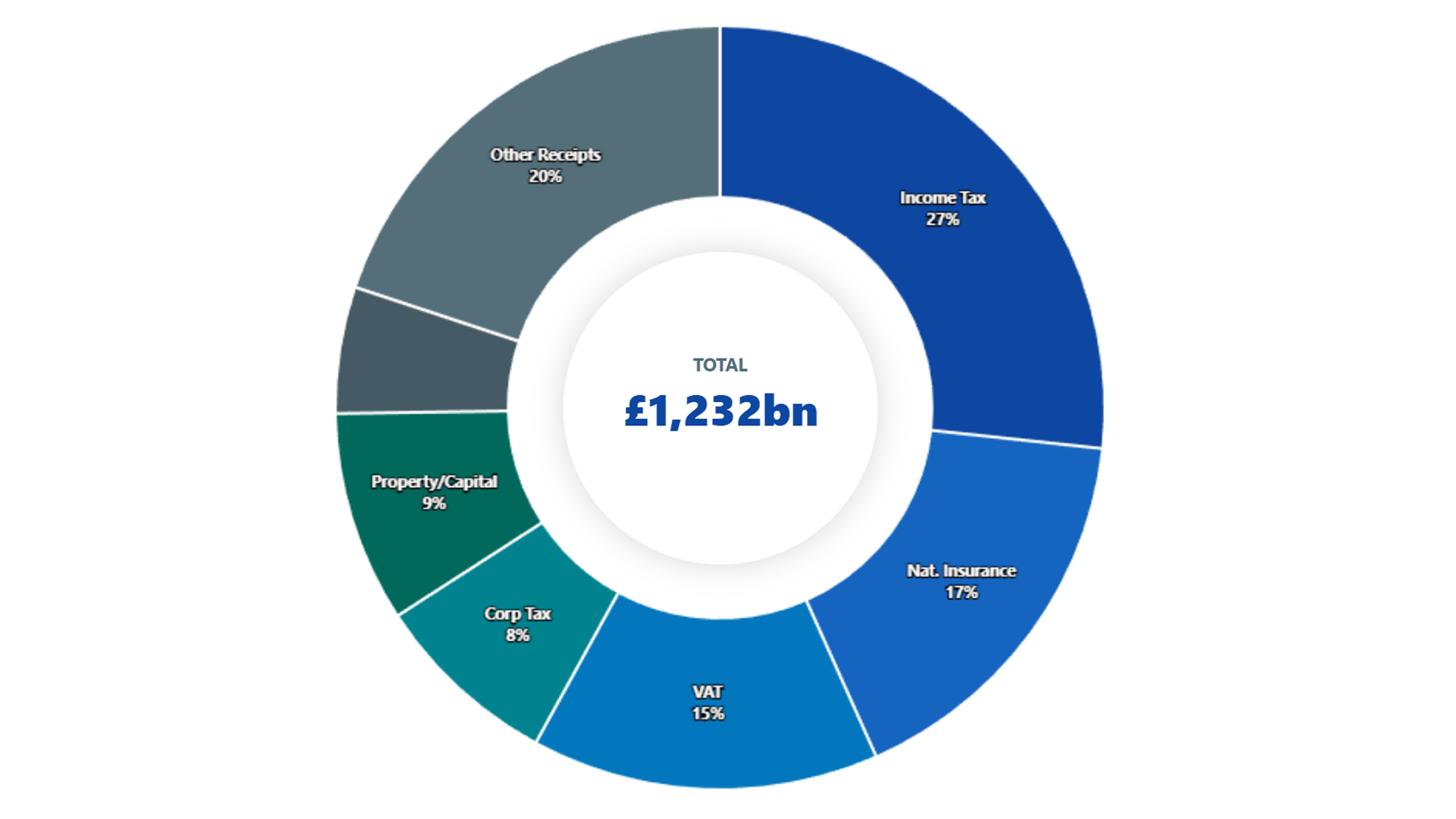

To understand the UK’s public finances, one must look at both sides of the ledger simultaneously. For the 2025/26 financial year, the Office for Budget Responsibility (OBR) forecasts that the government will collect £1,232 billion in taxes and other receipts, but it plans to spend £1,295 billion.

The Fiscal Trade-Off

Hover or tap any block below to see exactly what your taxes pay for—and what our national costs consume.

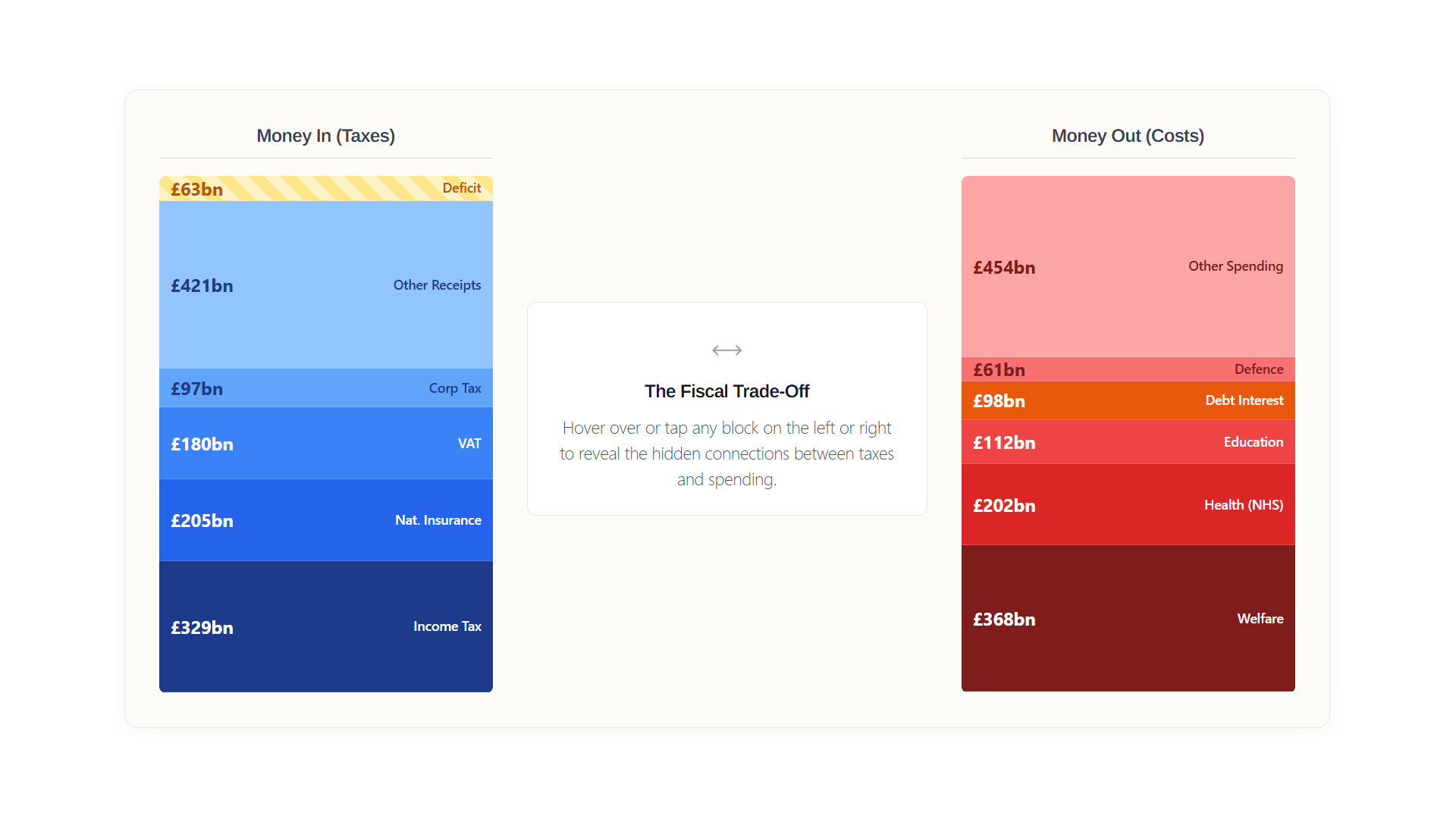

Money In (Taxes)

Explore the Budget

Hover over or tap any block on the left or right to reveal the hidden connections between the taxes we pay and the public services they fund.

Money Out (Costs)

The difference between these two figures leaves a shortfall of approximately £63 billion.

This gap is not an anomaly caused by a sudden economic shock like a pandemic or a financial crisis. Instead, it represents a structural deficit—a persistent imbalance between what the modern UK state is mandated to provide and what the current tax system is capable of raising.

By putting the receipts and spending data side-by-side, the underlying mechanics of this £63 billion shortfall become clear. It is the result of a “revenue ceiling” meeting an “expenditure floor.”

The Revenue Ceiling: A Concentrated Tax Base

The UK tax system is highly effective at raising capital, with the overall tax burden forecast to reach a post-war high of roughly 38.3% of GDP. However, the data reveals that this revenue relies heavily on a narrow demographic foundation.

- Heavy Reliance on Income Taxes: Income Tax and National Insurance combined account for over £530 billion—nearly 45% of all government revenue.

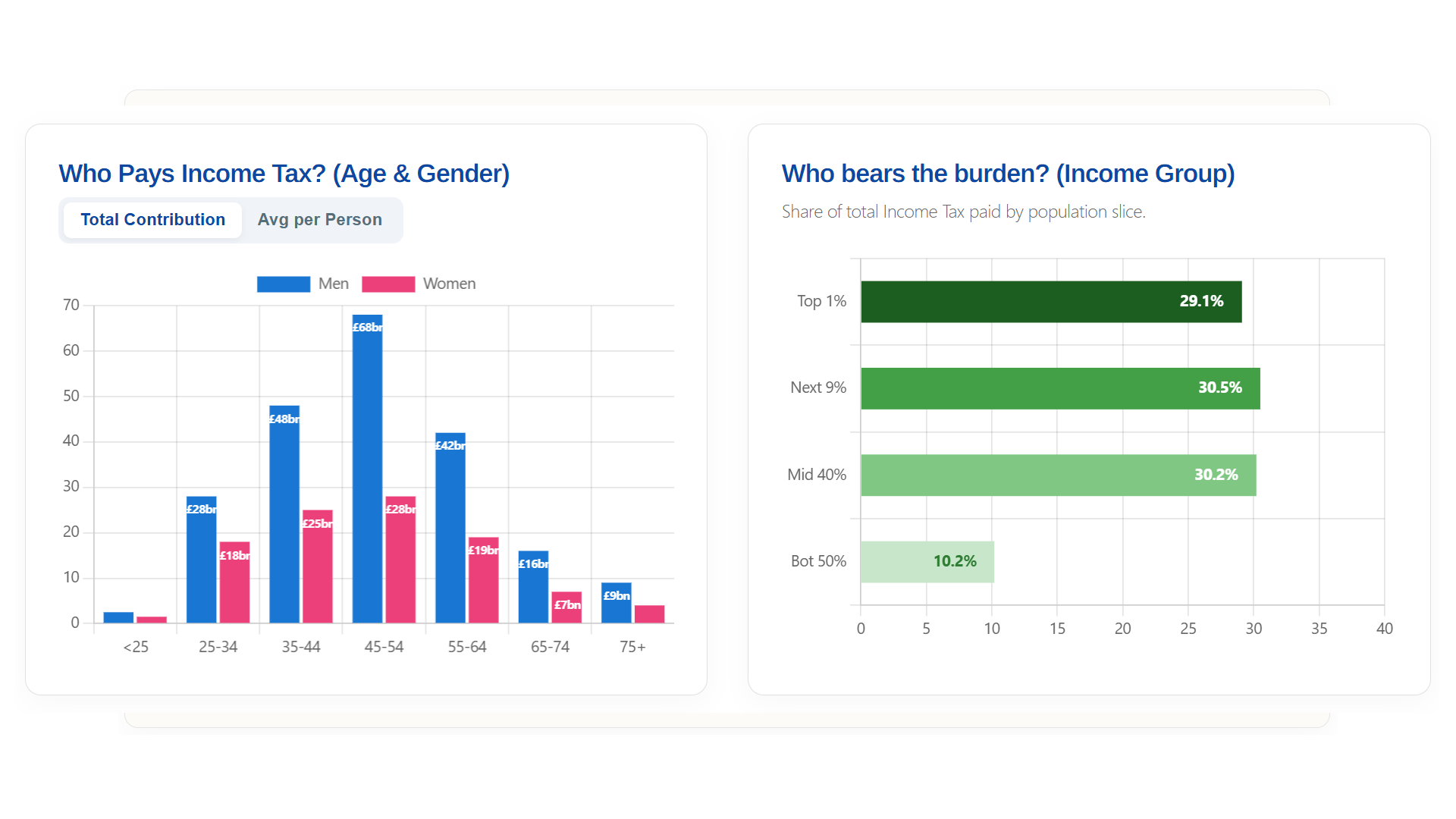

- A Top-Heavy System: As demographic data shows, the vast majority of this revenue is generated by a small percentage of high-earning, working-age individuals. The top 10% of earners contribute roughly 60% of all Income Tax.

This concentration creates a “revenue ceiling.” Governments face significant political and economic friction when attempting to raise taxes further on this small group of high earners. Conversely, attempting to broaden the tax base by raising taxes on the lower-earning majority—either through basic rate Income Tax hikes or increasing indirect taxes like VAT—carries heavy political risks and disproportionately impacts the cost of living for poorer households.

The expenditure floor: The cost of demographics

While revenue generation is constrained, public spending is subject to relentless upward pressure, creating a rigid “expenditure floor.”

- The Dominance of Health and Welfare: Combined, Welfare & Pensions (£368bn) and Health (£202bn) consume roughly 44% of total public spending. Unlike capital investments (such as building roads or railways), these are day-to-day statutory obligations.

- The Aging Population: Both of these massive budgets are intrinsically linked to demographics. An aging population guarantees year-on-year increases in State Pension costs (further amplified by the “Triple Lock”) and structurally higher demand for NHS and social care services. These costs rise independently of economic growth.

The compounding cost: Debt interest

When the expenditure floor exceeds the revenue ceiling, the government must borrow money from financial markets by issuing government bonds (gilts) to fund the £63 billion difference.

This borrowing is where the structural deficit becomes a compounding issue.

Because the UK has run a deficit for most of the last two decades, it has accumulated a substantial national debt. Servicing this debt is now one of the largest single line items in the budget. At £98 billion for 2025/26, debt interest payments are significantly larger than the entire Defence or Public Order budgets, and nearly equal to the Education budget.

Crucially, this £98 billion does not buy new hospitals, fund schools, or build infrastructure—it merely services past borrowing. When a government must borrow just to pay the interest on previous borrowing, fiscal flexibility is severely limited.

The Fiscal Trilemma

The £63 billion gap between the £1,232bn coming in and the £1,295bn going out illustrates a fundamental fiscal trilemma facing policymakers. To close a structural deficit, a government ultimately has only three levers to pull:

- Raise Taxes: Further increase the tax burden on a historically highly-taxed population, risking economic stagnation or capital flight.

- Cut Spending: Reduce the scope of the state, which is politically difficult given the aging population and existing pressures on the NHS and welfare system.

- Accept the Deficit: Continue borrowing to bridge the gap, accepting that a growing share of future tax revenue will be diverted away from public services to pay debt interest.

Without sustained, rapid economic growth to organically boost tax receipts without raising tax rates, the UK’s public finances will remain a delicate balancing act between these three difficult choices.