“International students in the 2021/22 cohort contributed a net £37.4billion to the UK economy over their study duration. This represents a huge return on public and institutional investment.”

Report for Higher Education Policy Institute & Universities UK

The UK is a world leader in higher education, but its business model has struggled in recent years because its main revenue stream, tuition fees, has been frozen at 2018 levels. It equates to a drop in real terms income of about 30%. However, given the world-class status of our institutions and a highly lucrative second revenue stream based on international students, there exists huge growth potential.

Would a sensible person be interested in:

- Leveraging one of our leading industries for growth, improved trade deals, and access to an enlarged pool for emerging, in-demand skills?

- Regeneration and thousands of jobs for 24 deprived areas/towns, generating improved government finances?

- A £9 billion improvement in the UK trade deficit?

What you need to know:

The UK is already a world leader in further education, with 12 universities ranked in the top 100 worldwide. Oxford has been ranked first for the last 9 years(1). The QS World University Rankings 2025 studies 1,500 universities from more than 100 countries. With 90 ranked institutions, the UK is second behind the US (197), with China in third with 71(2).

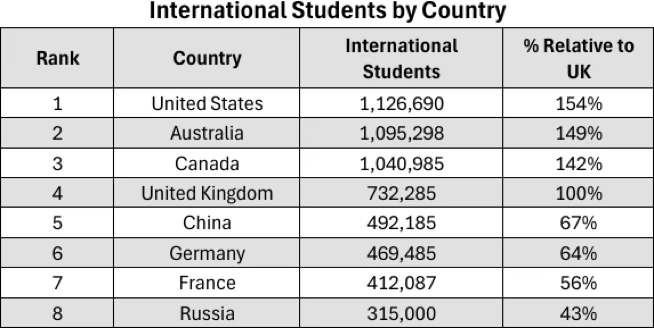

The number of people in UK higher education has risen from 2.1 million in 2000 to 2.9 million in 2023(3). Of these, 732,285 were international students; 656,735 were from non-EU countries, and 75,550 were from EU member states. 51% of international students are from India, China and Nigeria.

Global enrolment of approx. 100 million in 2000 rose to 235 million in 2020(4), meaning the UK market share of students has halved from 1.5% to 0.85%. If this were a business (which it is), it would be addressed.

The UK does well with international students (we have 68% of the US total despite having only 20% of the population, and well ahead of France and Germany – see table), but we are behind other, smaller, English-speaking countries (Canada and Australia).

Demand from more foreign students remains high, and is further helped by the confrontation between the Trump Administration and leading US academic bodies. British universities vary in size, with 51,435 at UCL; 46,915 at Manchester; 27,160 at Oxford; 38,100 attending Leeds; 21,750 at Durham; and 8,320 at Aberystwyth(5).

What to do?

- Building on existing educational leadership and reputation, take, say, 24 of our top institutions. Have each one build a new, remote campus for approximately 12,500 students each, creating a total of 300,000 new places. Growth of 10% on current total student levels, but 40% growth of (more lucrative) international students.

- With local authorities bidding for investment, select 24 deprived areas for the campuses. Investment in regeneration, facilities, and infrastructure creates jobs and stimulates the local economy. Weighting is given to those areas with a high density of existing, empty homes.

- Numerous academic roles will be created, but far more jobs will be created to support their work and the students — many of those roles would be relevant to the very people on welfare we are looking to convert to employment in the earlier chapter

For every £1 of public money invested in universities, £14 is returned to the UK economy. The total economic impact of teaching, research, and educational exports is estimated at £265 billion per year.— London Economics, commissioned by Universities UK**

- Focus each campus as centres of excellence in skills and sectors in demand in the UK (and internationally) — healthcare, medical research, biosciences, AI, engineering, technology, space, etc.

- These new campuses would primarily cater for international students.

- Target those countries with whom we want closer relations and/or an improved trading relationship, such as India, Brazil, Saudi Arabia, Korea, etc. Indeed, the UK/India Trade agreement was delayed because succes- sive British governments wanted stricter visa requirements for students. Lack of clarity over UK intentions is one reason why Confirmation of Acceptance for Studies (CAS) fell by 20% between 2023 and 2024 from 140k to 111k, and the number of international students accepting postgraduate places at UK universities dropped by 37% in January 2024 compared to the previous year(6).

The results

- Attract academic staff and students in key sectors our country and economy are interested in, now and for the future.

- International undergraduate fees typically range from £10,000 to £26,000+ per annum, and average student living costs are around £1,104/month. With approximately 300,000 foreign students, even if only a portion pay full fees, the UK could receive up to £9 billion per annum from tuition alone. Given a £45–50 billion trade deficit, this represents a 17–20% improvement in the net balance.

- 24 deprived areas regenerated with jobs created during the rebuild. Once operational, 12,500 students, plus say 2,500 staff in each location spend- ing a conservative £6k per annum, is £90m going to local bars, restaurants, supermarkets, etc., creating ongoing jobs and further investment.

Leverage in negotiating trade deals

- UK PLC and funding partners get first access to graduates with in- demand skills.

- UK PLC benefits from patents and innovations. It also becomes a more attractive location for international companies looking for a reliable flow of skills.

Why don’t we do this already?

Is it only the British that take global leadership and sacrifice it (time and again) on the altar of poor policy derived from political cowardice? We’re desperate for growth and to convert record numbers on welfare into work, but recent governments are actually reducing international student numbers. It means the jobs and revenues go to our competitors. Bonkers. The reason can be found in a lack of political courage, allowing the politically toxic topic of migration to stifle political ambition.

Net UK migration in 2023 was estimated at 900,000. International students and their dependents are included in these numbers. Instead of making the argument for growth, regeneration, jobs, an abundance of future skills, etc., it has been politically expedient to restrict international students with policy changes becoming effective from January 2024. This has led to a decline in international student numbers, with sponsored study visas falling by 14% in 2024(8). Applications for sponsored study visas decreased by 28% in June 2024 compared to the prior year 2023, so instead of thriving, many of our institutions are facing financial crises.

What to do?

With immediate effect, students and their families should be removed from the migration figures, treating them more like long-term, economically beneficial tourists. Given their areas of study, they will be in high demand. If roles exist in the UK, we would be mad to let them go, and at this stage, they and their dependents can be considered to have ‘migrated’ to the UK. We’d be glad to have them, and it would be cause for celebration. If not, they leave with our best wishes, and the UK has a network of highly skilled alumni across the world.

How to pay?

Significant annual savings have been found in the first two chapters; if all other funding options fail, some of these can be repurposed. Prune to grow. Before that, we can review options from foreign government sovereign wealth funds and corporate beneficiaries of the skill base, local authorities, as well as the 24 selected universities themselves. All would benefit from this investment.

References

- TimesHigherEducation(2024). ‘World University Rankings’ Available at: https://www.timeshighereducation.com/world-university-rankings/ latest/world-ranking

- Top Universities (2025). ‘Top Universities Ranking’. Available at: https://www.topuniversities.com/world-university-rankings

- HESA, (2025). ‘Who’s studying in HE?’ Available at: https://www.hesa. ac.uk/data-and-analysis/students/whos-in-he#numbers

- Atherton, G., Lewis, J., Bolton, P. (2024). ‘Higher education around the world: Comparing international approaches and performance with the UK.’ Available at: https://commonslibrary.parliament.uk/research– briefings/cbp-9840/

- HESA (2024). ‘Where do HE students study?’ Available at: https://www.hesa.ac.uk/data-and-analysis/students/where-study

- Financial Times (2024). ‘UK universities hit by fall in overseas students taking up postgraduate places.’ Available at: https://www.ft.com/conte nt/147e8b89-a340-4367-9ada-8f197afb0bfd

- Save the Student (2024). ‘UK tuition fees for international students.’ Available at: https://www.savethestudent.org/international-students/ international-student-fees.html

- ICEF Monitor (2025). ‘UK: Reduced demand from India, Nigeria, and Bangladesh drive a 14% decline in sponsored study visas in 2024.’ Available at: https://monitor.icef.com/2025/03/uk-reduced-demand– from-india-nigeria-and-bangladesh-drive-a-14-decline-in-sponsored-study-visas-in-2024/