On 22nd February, The Sunday Times reported that the Conservative Party will back efforts to reduce the high interest rates faced by those on Plan 2 student loans. On its own terms, that is welcome. A system in which balances can rise for years despite regular repayments has always felt morally questionable.

But while Westminster debates the interest rate on a £236 billion student loan book, it remains largely silent about a £2.8 trillion national debt — and more than £100 billion a year in interest payments — that today’s younger taxpayers are expected to service.

We are having the wrong argument.

Student debt is visible. It appears on statements. It is personalised. It feels unfair. National debt is invisible. It does not arrive in the post. It has no repayment schedule pinned to the fridge. And yet it is vastly larger, perpetual, and structurally more significant.

Graduates may bristle at watching their student loan balances grow. But many do not yet realise that they — alongside other working-age taxpayers — will spend decades financing sovereign borrowing accumulated long before they earned their first payslip.

The debate about student loans is loud and emotive. The relative silence on controlling national debt is striking

Only one of these liabilities will shape the fiscal landscape for the next half-century.

Whilst reducing student loan interest may ease a grievance, failing to confront the scale and trajectory of national debt means quietly passing a far heavier burden to the same generation.

If we are serious about intergenerational fairness, we cannot tweak the edges of student finance while ignoring the main event: the long-term fiscal inheritance being handed, with minimal consultation, to younger taxpayers

If that sounds dramatic, it shouldn’t.

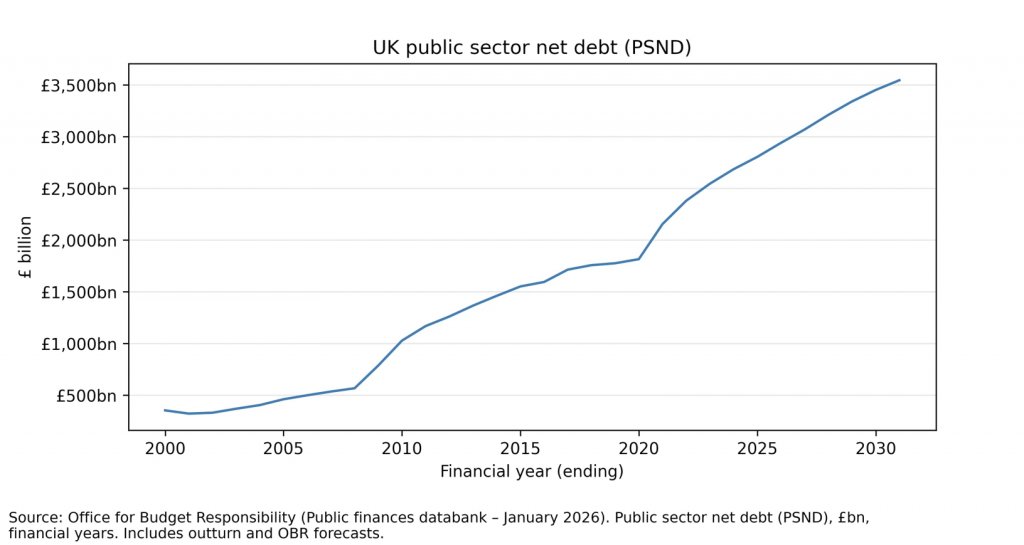

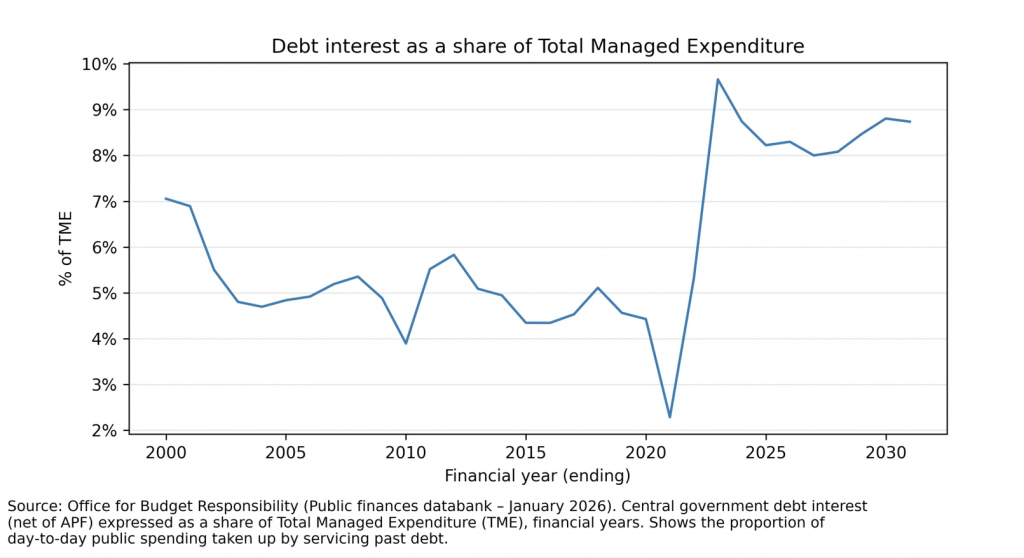

This is not an abstract moral complaint. It is a matter of scale and arithmetic. The UK’s public sector net debt now stands at approximately £2.8 trillion, close to 100% of GDP (Office for Budget Responsibility, 2025). Annual debt interest payments exceed £100 billion — more than we spend on defence and approaching the size of the annual education budget.

Put differently: before a single nurse is paid, before a road is repaired, before a classroom is funded, over £100 billion must be found simply to service past borrowing. That’s almost 10% of total government spending, a figure that continues to grow, and the bigger the debt, the less control we have over the level of interest rates we can borrow at.

Student loans may feel burdensome because they are personal. National debt is more burdensome because it is structural.

Student loans expire. National debt rolls forward — is refinanced, reissued, and accumulates.

And while the student loan debate focuses on whether balances are rising too quickly, the national debt continues to grow through persistent borrowing averaging around 4–5% of GDP over the past two decades (House of Commons Library, 2025). If fairness is the test, we need to ask a more uncomfortable question:

Not just “Are student loans too expensive?”

But “Who will finance £100 billion a year in debt interest — and for how long?”

Because unlike student debt, this liability does not disappear after thirty years.

It becomes the fiscal weather in which the next generation must live.

Demographics only make the matter worse for our kids

Unfortunately, the story does not end with the size of the debt – it gets harder when we consider who is left to pay it.

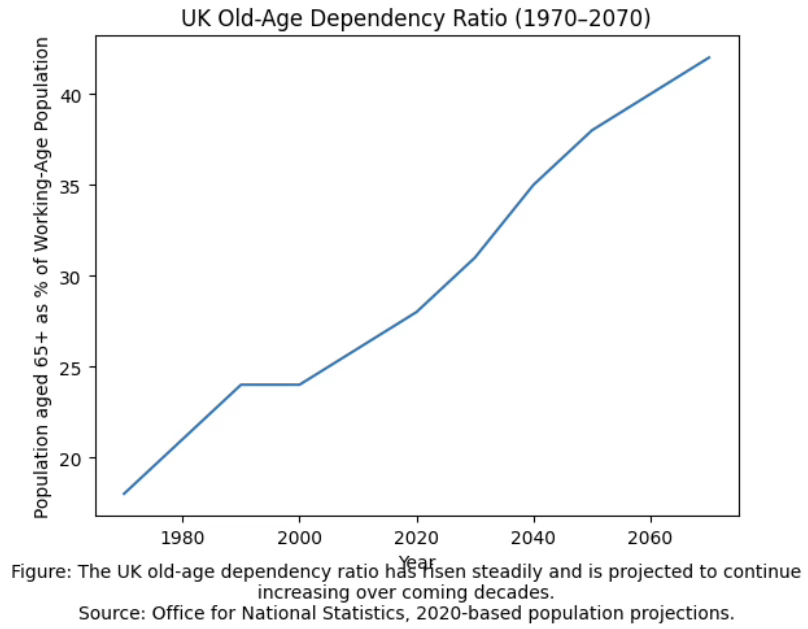

The UK’s fertility rate has fallen to around 1.5 children per woman, well below the replacement rate of 2.1 (Office for National Statistics, 2024). At the same time, life expectancy has increased over the long term, and the population is ageing rapidly. The Office for Budget Responsibility’s Fiscal Sustainability Report makes this clear: spending on state pensions and healthcare is projected to rise steadily as a share of GDP over coming decades, driven largely by demographics rather than political ideology.

Fewer workers. More retirees. In 2000 there were roughly four working-age adults per pensioner; that ratio is projected to fall towards two over coming decades (OBR Fiscal Sustainability report).

National debt is often expressed as a percentage of GDP. But GDP does not pay taxes. People do. If the number of working-age taxpayers grows more slowly than the stock of debt — or even declines — then the implicit burden per worker increases. Even if debt stabilises relative to GDP, a shrinking worker-to-retiree ratio means each worker carries a larger share of financing both age-related spending and debt interest.

And here is where the intergenerational imbalance becomes unavoidable:

The commitments were made in the present.

The servicing burden falls into the future.

Student loans are debated intensely because they are personal and immediate – National debt is tolerated because it is collective and delayed.

But delay does not eliminate obligation. It simply shifts it. And with fertility below replacement, and every major political party committed to lower net migration than recent peaks, the pool of future taxpayers is unlikely to expand dramatically. Which means the share borne by those already in — and about to enter — the workforce grows heavier.

This is not conjecture. It is arithmetic.

The question is unavoidable: who ultimately finances the future?

Demography tells us the burden is rising.

Tax data tells us who is likely to carry it.

National debt is serviced through taxation, but taxation in the UK is not evenly distributed.

According to HMRC’s most recent Income Tax Statistics (2024):

- The top 10% of income taxpayers contribute around 60% of all income tax receipts.

- The top 1% contribute close to 30%.

That concentration matters. The burden of servicing national debt falls disproportionately on higher earners — who are, on average, working-age taxpayers. Meanwhile, a significant and growing share of public spending is directed towards age-related commitments such as pensions and health care.

The result is not a moral judgment, but an arithmetic reality: the cohort contributing most to debt servicing is not the cohort benefiting most from age-related expenditure.

Income tax remains the single largest source of government revenue. Add National Insurance, VAT (which rises with higher spending), and taxes on savings and investment, and the fiscal system depends disproportionately on higher earners, and graduates are overrepresented in that cohort.

Office for National Statistics data consistently shows a significant lifetime earnings premium associated with degree-level qualifications (ONS Labour Market Statistics, 2024). Not all graduates are high earners. Not all high earners are graduates. But graduates are disproportionately present in the income bands that fund the majority of the Exchequer.

Which means that when the government spends more than £100 billion per year on debt interest, it is not an evenly shared cost. It falls most heavily on those earning the most — and those most likely to be in sustained employment over decades.

This is why the student debt debate is incomplete.

A graduate may see a rising student loan balance and feel aggrieved. But that same graduate is also disproportionately represented among those financing sovereign debt servicing through income tax, National Insurance and indirect taxation.

And this is not only about graduates.

Younger workers — graduate and non-graduate alike — are the ones in work today and tomorrow. They are the tax base upon which both age-related spending and debt interest depend. Older cohorts may have benefited from decades of expanding public services financed partly by borrowing. Younger cohorts will finance the servicing.

That is the intergenerational transfer.

It is not contractual like a student loan. It does not appear on a statement. But it is economically real.

Student debt is debated because it feels unfair at the individual level.

National debt deserves scrutiny because it is becoming increasingly unfair at the generational level.

Even the politics is against younger generations

And this is where an uncomfortable political reality enters. Public finances are not just numbers. They are the product of incentives. Older voters are significantly more likely to vote than younger voters. Electoral data consistently shows turnout rising sharply with age and Governments, rationally, respond to those most likely to turn out.

The result is a structural bias in policymaking:

- Protect existing entitlements.

- Protect pensions.

- Protect age-related benefits.

- Avoid sharp fiscal adjustments that impose immediate pain.

Borrowing becomes the release valve.

It allows governments to maintain current commitments without immediately raising taxes or cutting spending. It spreads the cost forward — beyond the current electoral cycle.

But spreading cost forward is not eliminating it.

It is shifting it.

And when borrowing becomes structural rather than exceptional — when deficits persist outside of crisis periods — that shift becomes generational. This is not a moral accusation against older citizens. Many pensioners are not wealthy. Many rely entirely on state provision.

Nor is it a partisan point. Governments of different political colours have contributed to the same trajectory.

It is an observation about democratic incentives that risks leaving the next generation exposed to fiscal constraint

If the political system rewards the protection of present benefits more than the preservation of future fiscal capacity, then debt accumulation becomes politically easier than reform.

Student debt is visible, targeted and electorally salient.

National debt is diffuse, delayed and politically tolerable.

But delayed costs do not disappear. They compound. And the compounding burden settles most heavily on those who will be working — and paying tax — for the longest period ahead.

That is not ideology. It is the logic of democratic finance under demographic pressure.

The double and triple whammy on younger taxpayers

All of this might still feel abstract.

It isn’t.

Younger working-age adults today face a combination of pressures that no recent generation has encountered in quite the same configuration.

First, earnings growth. Real wage growth over the past 15 years has been historically weak by UK standards (ONS Earnings Data, 2024). For much of the post-financial crisis period, real earnings stagnated. Even with recent nominal increases, living standards for younger households have not risen at the pace seen in previous decades.

Second, housing. The ratio of house prices to earnings has more than doubled since the 1990s (ONS Housing Affordability Statistics). For many younger workers, housing costs — whether mortgage or rent — consume a significantly higher share of income than they did for earlier generations at the same stage of life.

Third, taxation. The UK tax burden is now at its highest sustained level in post-war history, approaching 37–38% of GDP (OBR, 2025). Freezes in income tax thresholds mean that more of each incremental pay rise is captured by the state — a phenomenon known as fiscal drag.

For graduates, there is a fourth layer: student loan repayments of up to 9% above threshold income. For many middle-income earners, this operates effectively as an additional marginal tax. A graduate earning £50,000 can face an effective marginal rate above 50% once income tax, National Insurance and student loan repayments are combined

Add these together and the picture becomes clearer:

- Slower real wage growth

- Higher housing costs

- High and rising effective tax rates

- Student loan repayments (for many)

- And the long-term obligation to service national debt

Those who did not attend university are part of this equation. National debt is serviced collectively. It is financed through income tax, National Insurance, VAT and business taxation — all of which ultimately rest on the working population. In short, today’s younger taxpayers face both personal and structural obligations.

Student debt is visible and time-limited. National debt is invisible and open-ended.

One expires after 30 or 40 years. The other becomes part of the fiscal environment for the rest of their working lives.

The burden is not merely that younger cohorts will pay more. It is that they will pay more while starting from a weaker asset base — lower home ownership rates, higher entry housing costs, and slower early-career income growth than previous generations experienced.

That is the intergenerational imbalance. Not because older citizens are to blame. But because the structure of public finance has evolved in a way that concentrates obligations on those with the longest remaining working lives.

The Fairness Test

If we are prepared to debate whether student loan interest is fair, we should apply the same test to national debt. Student loans produce headlines. The National Debt produces more than £100 billion a year in interest payments. If fairness is the standard, then we must ask:

- Is it fair to run persistent deficits outside of crisis periods?

- Is it fair to finance current consumption through borrowing that future workers must service?

- Is it fair that younger taxpayers — graduate and non-graduate alike — shoulder both rising taxation and rising debt interest while facing weaker asset accumulation than previous generations?

Reforming student loan interest may improve fairness within higher education, but it does not address the structural imbalance embedded in the national balance sheet.

The Structural Reality

The UK’s fiscal position is not merely a snapshot. It is a trajectory:

- Debt approaching 100% of GDP.

- Interest payments exceeding £100 billion annually.

- Age-related spending rising as a share of national income.

- Fewer workers per retiree.

These are not ideological claims. They are drawn from the Office for Budget Responsibility, the Office for National Statistics and the Institute for Fiscal Studies.

The question is not whether student debt is imperfect. The question is whether we are willing to acknowledge that sovereign debt, compounded over decades, may represent a far greater intergenerational transfer.

Debt does not disappear because it is refinanced. Interest does not vanish because it is paid collectively. Arithmetic does not soften because it is politically awkward.

The Conversation We Need

This is not an argument against pensioners.

Not an argument against welfare.

Not an argument against supporting students.

It is an argument that modest adjustments to student finance will not resolve a much deeper fiscal inheritance.

If we continue borrowing at scale to sustain present commitments, younger taxpayers will face:

- Debilitating interest payments,

- Constrained public services,

- And reduced fiscal flexibility in the next crisis.

Student debt reform may ease a grievance, but it does not confront the main event.

Intergenerational fairness demands that we widen the debate from tuition fee interest rates to the sustainability of the national balance sheet. Until we do, we are not fixing the problem.

We are adjusting the symptoms.