“You cannot keep borrowing indefinitely without consequences — markets eventually react and react harshly.”

Roger Bootle, economist and Telegraph columnist

Our political masters have failed to be transparent with the British public over one inescapable fact: the UK cannot afford to maintain current spending levels.

I wish we could, but we can’t.

Most chancellors make it part of their central pitch to restore the nation’s finances. ‘Rules’ are created about borrowing and investment. Upon announcement, they are invariably described as ‘ironclad’, ‘strict’ and ‘realistic’.

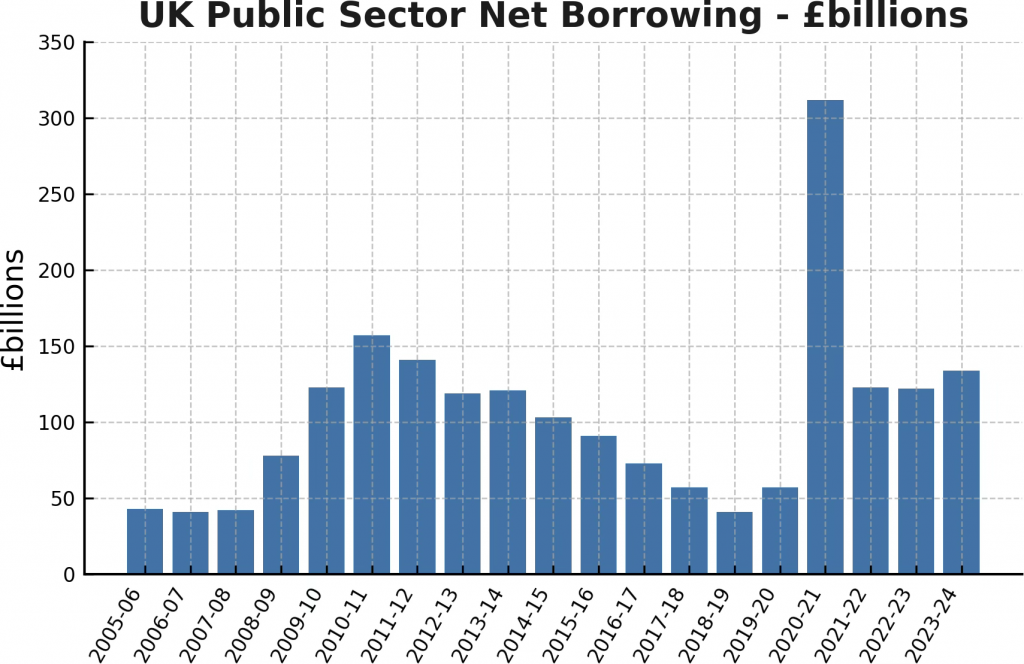

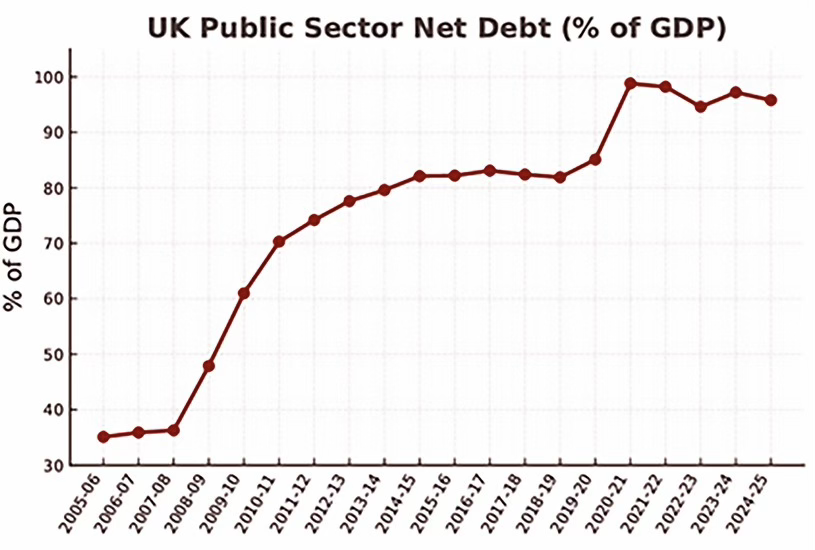

As the two graphs below illustrate, what they can’t be described as is effective.

UK public sector net borrowing figures since 2005

UK public sector net debt figures since 2005 as a percentage of GDP

All countries, like most people and businesses, have debt. Our problems are:

- The current level of debt compared to GDP

- Relentless borrowing (making the debt pile bigger)

- Spending that borrowing to pay for day-to-day expenditure, and not investment

- Growing interest payments

- There’s no plan to pay it back — ever.

This model would never work for an individual or business, but at a national level, there is a collective denial and assumption that this is somehow standard practice. We can kid ourselves, but older readers will have experienced the humiliation of a visit from the IMF. Voters can vent all they like about entitlements, but 1980s austerity put 3 million people out of work in a population almost 20% smaller than today’s 68 million. When Roger Bootle talks of markets ‘reacting harshly,’ this is just a taste of what we might expect.

Let’s look at some numbers:

- Current national debt: In the full financial year 2023/24, public sector net debt was about £2.7trillion, representing roughly 96% of GDP. That’s £2,700,000,000,000 or £39,700 per man, woman, and child in the country.

- In 2000, the debt was £353 billion or 30% of GDP. With a population of 59 million, everyone’s share was just £5,983. Just what have we all got for the additional £2.4 trillion?? Potholes, sewage in rivers, crises in almost every area of public service, and the most vulnerable are on the precipice.

Not only does this model not work, but it’s worse than you think:

- The debt keeps going up because of government borrowing. The finger is pointed at ‘exceptional’ crises, but their frequency suggests there is nothing exceptional about them. In the two full financial years since the COVID crisis, borrowing averaged more than £100 billion per year — an additional £1,500 per person, per year

- Borrowing has fluctuated over the last 20 years at an average of 4.9% of GDP(4), yet the next fiscal crisis is already here, with an unfunded additional requirement for defence spending to reach 5%.

“We have to deal with our debts. If we don’t, there will be no growth, no jobs, no prosperity.”

David Cameron, 2010

The real killer is the interest payments (which we never seem to hear anything about).

Annual net interest payments have exceeded £100 billion in each of the last three years, now accounting for 8.7% of total government spending. That’s £1,600 per person (up from £474 in 2000). In short, we’re borrowing almost the exact same amount as we pay in interest. Insane, but true. In populist speak, it’s enough to pay for more than 2.1 million nurses.

This means that for each of the 1,800 babies born today, their lifetime bill for interest on our debt to fund our spending would start at £141,617 — if we didn’t borrow another penny — from the day they were born(8). Welcome to Britain.

“Society is a partnership not only between those who are living but between those who are living, those who are dead, and those who are to be born.”

Edmund Burke

Lumbering our children and grandchildren with our debt isn’t just unfair, it’s immoral. Most sensible people want to pass an inheritance on to the next generation. Despite our best attempts to run this country down, we will bequeath them a free, fair and tolerant country with education, healthcare and opportunity that most countries cannot match. But approximately £150k and counting feels ‘toppy’ to cover what their parents and grandparents felt entitled to. It’ll get worse as demographic changes see the interest burden shared across fewer workers.

If nothing changes, the economy will need to be 9% larger to eliminate the need for any further borrowing. If we can rediscover the political will and ambition, this is possible over the medium term (3-10 years), but reining in current and future spending in the short term (1-3 years) is critical to bridge the gap, invest in growth initiatives, and fund the next crisis. I repeat — I don’t believe in debates about cuts — I believe in rethinking government policy, one that places a premium on living within our means and protecting the most vulnerable. Then we can set about growing the economy. Prune to grow.

Unfortunately, yet again, things are worse than we think. We measure debt in terms of its relation to GDP, but GDP itself is a limited tool. The country has grown since the financial crisis — it might be anaemic, but it’s still growth. So why do most people not feel richer? With GDP being a blunt instrument, the pie has grown, but the population has grown at a faster rate. Measured in GDP per capita, our position looks far less rosy.

Our national debt suffers from the same comparison. We compare it to GDP, but what if we compare it on a per capita basis for the people paying the interest, aka the taxpayer? The population has grown dramatically in recent years, driven by record migration, but all governments are committed to turning off this tap, suggesting a fall in employment numbers. This means fewer workers paying into the pension pot must, in turn, pay for more pensioners and shoulder more of our debt at interest rates we do not control.

Those workers we’re talking about are our children.

We must rethink the current arrangement. Simply put, a large part of the answer lies in ‘prune to grow,’ which I argue is the basis for how we’ll improve the economy and the government’s fiscal position.

First, we must bring spending under control to reduce borrowing. This ‘pruning’ means spending less, but what’s really required is a review of how we spend. I will share some back-of-the-napkin solutions to save tens of £ billions across two areas — pensions and welfare, but whilst anyone can identify ‘cuts,’ it’s the how that’s crucial. We pay billions based on a system created 80 years ago. It worked then, but it doesn’t work now. Rethinking these areas means spending more to protect and support the most vulnerable, spending less on those that don’t need it, and fostering a new attitude towards the purpose and degree of welfare.

Then we’ll look at some solutions using some of our reduced spending to invest in growth. The goal is lower spending and faster growth — especially growth targeted at those areas most in need — as well as protection for the most vulnerable, all whilst offsetting the pain for those negatively impacted. At the same time, we could start a national conversation to significantly impact our position on net-zero, food and energy security, negotiation leverage for trade deals, improved balance of payments, and social justice.

Wherever possible, I have kept the research basic, as there’s only one of me and our overall position is clear for any sensible person to see. I will leave the details to others, but I look forward to the debate.

Just to be clear, I’m not saying this is how it should be done, but rather suggesting that some creative thinking can take the conversation mainstream to deliver some step change in our economic performance. And that these changes must not only protect the most vulnerable, but also improve their position. So that those who lose out in any changes can benefit from reallocated resources to help offset their pain.

The goal is a virtuous circle of an improving fiscal position that is ultimately paying for more and better-targeted public services.