“If I’d proposed solving the pension problem by compulsory euthanasia for every fifth pensioner, I’d have got into less trouble for it.”

Tony Blair

We’ve created a pensions monster. Mr Blair hasn’t been in power for almost 20 years, and yet, there was a problem then, and it’s just gotten worse, a lot worse. There’s waste and inefficiency across most areas of public spending, but the sums spent across pensions and welfare, whilst dizzying, offer the quickest route to right-sizing our annual borrowing costs.

Before we start, a quick reminder of a few caveats: I’m not saying this is how it should be done, but rather I’m offering some examples of how it could be done. The research is basic, but I believe materially correct, and all we want to do at this stage is start a mainstream conversation.

So, with that said, would a sensible person be interested in:

- Saving £27 billion per annum off the future state pensions bill?

- Real-term increases to the state pension for the poorest 70% of pension- ers?

- A fully funded, immediate £12 billion per annum tax cut to offset the pain and help get the economy going?

If so, then read on.

Background — what you need to know

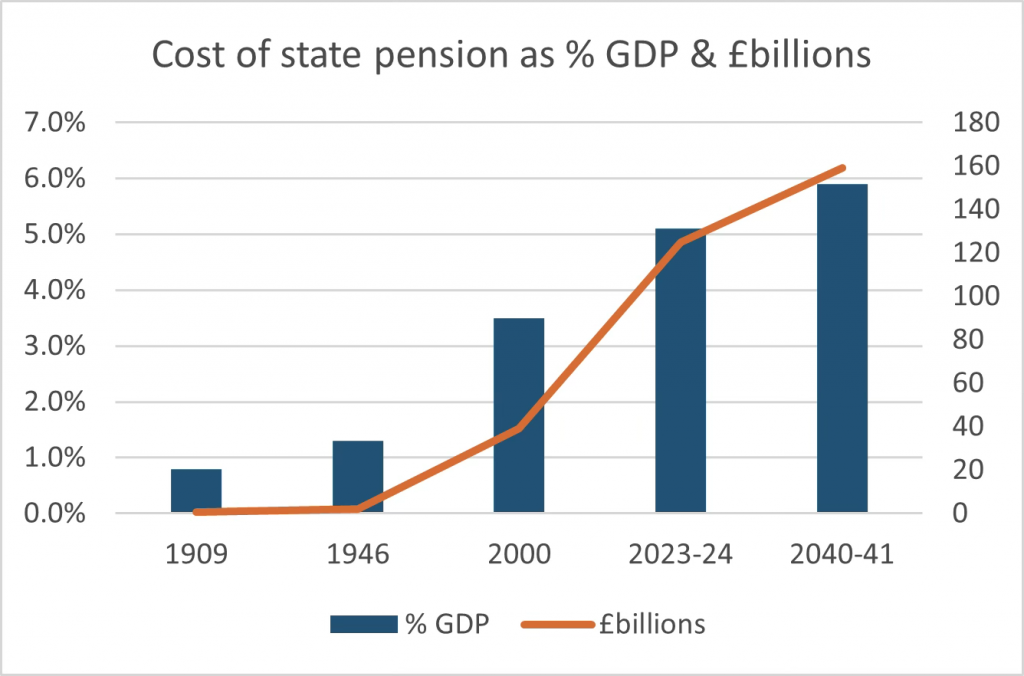

- 1909 — State pensions were launched. Means-tested. Available at age 70. 660 thousand people eligible(9). Adjusted to 2023 levels, the annual cost was £830 million or 0.48% of GDP(4),(1).

- 1946 — The National Insurance Act removed means testing and lowered eligibility age to 65 for men, and 60 for women(17). 4.5 million people became eligible. Annual cost was 1.3% of GDP(11).

- 2000 — 11 million eligible, but changes were in the pipeline to change the age. Annual cost was £39 billion or 3.5% of GDP(10)

- 2023-24 — Annual cost is £125 billion or 5.1% of GDP(10). The 23/24 state pension was worth £221.20 per week or £11,502.40 per annum(16). Current life expectancy for men is 79 years, and for women, 83 years(15).

- 2040-41 Annual cost predicted at £159 billion or 5.9% of GDP(13).

- Total pensioner costs to government (including health, social care) are set to rise from 15.4% of GDP (2022-23) to 18.7% in 2040-41(6).

- The current arrangement: Since April 2016, every pensioner receives £12,000 per annum if they have met the threshold of 35 years of NI contributions.

The problem

- The current arrangement is becoming more expensive every year com- pared to our ability to pay. The ‘triple lock’ increases pensions by the highest of 2.5%, annual wage increases and inflation. This means that unless annual GDP growth outpaces 2.5%, AND outpaces inflation AND average wage increases every year, pensions automatically become less affordable each year(12) as pensions would rise faster than inflation. Lord Willetts, President of the Resolution Foundation and former government minister, is excellent on this.

- There is an increasing disconnect between people’s expectations and what they will receive.

- To bridge the funding gap between what we have promised and what we can afford, taxation levels have risen to record peacetime levels, reaching 36.9% of GDP in 2023/24 (compared to an average of 32% in the early ’90s and 30% in the early 2000s(2)). Higher taxes paradoxically act as a drag on the very growth required to bridge the gap, so we still have to borrow £100 billion to pay the bills.

- Not only is it political suicide for any party to address this, but it’s in their interest to exacerbate the problem — showering more cash on those most likely to vote for them. This means that we, the voters, are as much to blame for our predicament as our political masters — older voters, for impoverishing future generations; and younger voters, for disenfranchising themselves by not bothering to turn out at the polling booth.

“When you spend someone else’s money on someone else, the incentive to be careful disappears — and that’s how governments create debt for the unborn.” — Milton Friedman

What to do?

- Outsource a long-term solution to an independent body and insulate political parties from any electoral fallout — the greater the insulation, the better the chances of success. Think of a grand bargain, or a wartime cabinet-style national consensus.

- An independent body could then have the required honest conversation with voters, without the political blowback.

The conversation would need to cover the following points:

- Being unaffordable and getting worse, the current system needs to be rethought, or else more dramatic changes will be forced upon us by the simple law of financial mathematics. Already, we see ‘the markets’ reacting to every suggestion connected to spending and the impact on debt, and if we don’t get our house in order, our borrowing costs will determine what we can and cannot do, not our elected representatives. It’s the very opposite of taking back control.

- People need clarity about what their retirement looks like:

- The state pension is there to support your retirement, not fully fund it.

- Supplementing the pension is the responsibility of the individual through savings or ongoing part-time employment

- Means-testing is already used for some benefits and should be applied to the state pension

- Reverse the current conversation. Not, “What do we want to give people?” but rather, “How much money do we want to allocate and what is the most equitable way to split it?”

- The size of the pension pot should reflect our ability to afford it. This would include freezing pension increases during recessions. In this way, everyone has a vested interest in growth and shares in any economic pain until growth is restored.

- Cutting costs is not the solution — anyone can suggest that. A rethink needs to improve the situation of the vulnerable and offset any pain for those losing out.

- You have not paid for your state pension. Any payments made via National Insurance are used to pay for current pensioners. This worked after 1946 when the number of workers outgrew the number of pensioners, but it doesn’t work now, and demographics will make the situation even worse

- The current arrangement is the single biggest argument for the increase in immigration — more workers to pay for more pensioners. This, in turn, has fuelled the rise of populist politicians in recent years. Migration can have significant benefits, but it kicks the pension can down the road, as ever more workers are required for ever more pensioners (as measured by the ONS as the ‘Old Age Dependency Ratio’).

- Using some of the money saved to offset pain for those losing out and to invest in other growth initiatives can fuel the economic growth that enables higher payments in the future. Prune to grow.

Here’s how

- Means Testing

- The clue is in the name. The tax we pay for our state pensions is called National Insurance. It’s there if you need it. If every insurance policy paid out, then the insurance industry would go bust. The case for means testing is already in place as it’s applied to other benefits. This could be applied in a way to make significant savings and increase support for the poorest pensioners.

- The following is purely an example to start a conversation. At pension age, we can divide people into segments. For ease, I’ve used deciles.

- The UK Govt. currently segments people for means testing based on income, savings, household composition and specific circumstances. Whatever method is finally agreed upon, people could be informed annually over their 45+ years of adulthood, providing clarity for retirement planning purposes.

- Agree on the net future impact on each decile — any changes would be far enough in the future to enable planning, and be phased or tapered in.

Table 1 (below) shows the proposed impact on the most well-off 30% at pensionable age.

- The 10% most well-off move towards zero pension (gradual loss of 100%)

- The next two deciles see their state pension gradually reduced by 50% and 25%

The changes would be far enough in the future for people to plan, and tapered so as to reduce as much friction as possible. As a conversation starter and as shown in the table above, the total savings on the pensions bill would be 17.5% or approximately £22 billion in the 2023/24 fiscal year, when total costs were £125 billion. The downside is the creation of a perverse dis-incentive to build lifetime financial independence, which is addressed later.

This example is not necessarily how it should be achieved, but rather an example of how means testing could be applied to right-size the cost of pension provision.

Let’s look at it another way.

At the time of writing, the combined wealth of the richest 10 people in the UK was just north of £200 billion. Most sensible people (probably including them) would agree that the approximately £12k per annum state pension could be better spent. Yes, they’ve paid into the system, handsomely, but they don’t need the ‘insurance’ to get by. We should celebrate wealth creators, thank them endlessly and work tirelessly to create more, but let’s deploy these financial resources more wisely.

If we agree on this point, the debate then shifts to where we draw the line and the extent of the impact. According to a recent study by the estate agent Savills, those over 70 have assets of just under £3 trillion in property alone. The Office for National Statistics reports widely on wealth, with suggestions of total wealth of those over 70 being between £5.8 and £6.6 trillion, with an estimated 700,000 of the over 70s owning assets over £2 million(18). As you would expect, this sum is not split evenly across deciles. Means testing identifies those less in need. Then we apply taper reductions accordingly.

Assuming a saving as per the above, some of this could be reinvested to support both social justice causes and incentivise people to be as financially successful as possible, so that they want to be in our top 30%. Later, I will explore doing this through lower taxes, but first, let’s do the socially just thing by supporting the 70% most vulnerable pensioners.

In the table below, we see:

- The least well-off/most vulnerable 30% of pensioners all see an immediate increase of 10%

- The next 40% get a modest 5% increase

So, 70% of the most vulnerable pensioners get a boost, reducing our savings from 17.5% to 12.5% at just over £15.6 billion in nominal terms for FY 23/24.

Re-alignment of the link between pension age and life expectancy

What you need to know:

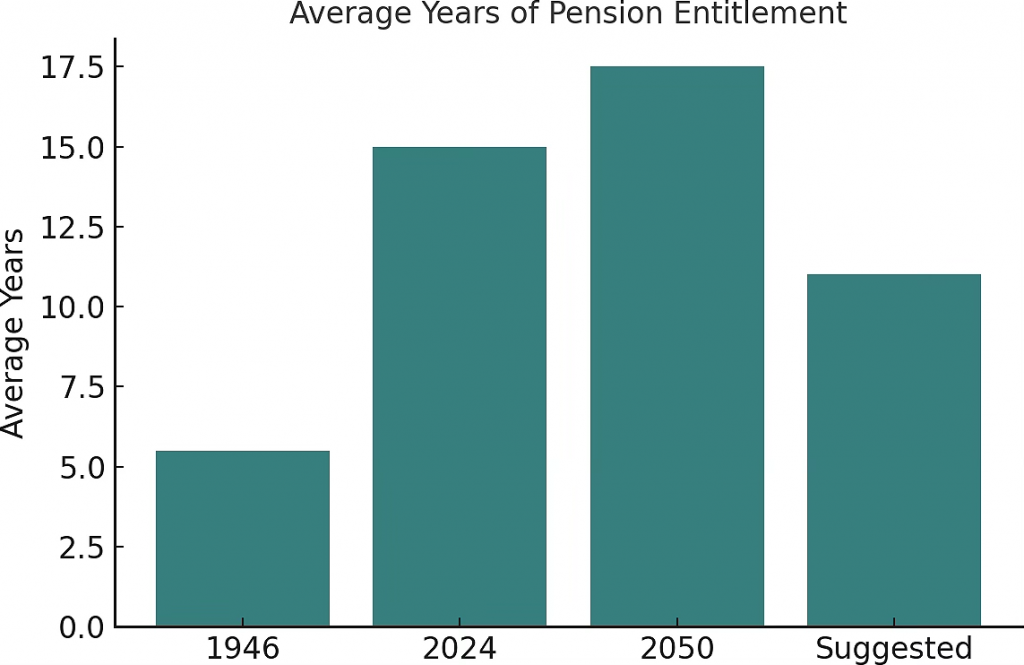

- The period over which someone is entitled to a pension has tripled. In 1946, life expectancy for men was 66 years and for women, 70(14). It meant that men could expect a pension for one year and women for 10 years, an average of 5.5 years. In 2023/24, with retirement age at 66 and an increase in life expectancy to 79 and 83 years, men can expect a pension for 13 years and women for 17 years, an average of 15 years(15).

- Although increases are planned to the retirement age, these are outpaced by projected life expectancy: Retirement age — to 67 between 2026-28; and 68 in 2044-46 (though this may be brought forward)(13). Projected life expectancy is expected to increase by 2050 to 90/91 for males and 92/93 for women(5)

- It means the average period of receiving a pension increases to approxi- mately 17.5 years, at the same time as a decrease in the number of children and grandchildren who bear the cost. Again, the current ‘solution’ of migration does not solve the problem; it only delays it, makes it bigger, and opens the door to populists.

- The IFS suggests that for each year the pension age is raised, £6 billion is saved per annum(7). The OBR quotes a figure of £10.4 billion improvement per added year, of which £0.9 billion comes from increased tax take as approximately 800k workers remain in employment.

- We could agree that the pension would support retirement for double the time envisaged in 1946, i.e. 11 years, rather than 5.5 years in 1946 (down from 15.5 years now and a projected 17.7 years by 2050). The age would move in line with any further changes to life expectancy.

- Increasing the age of retirement over time by the required additional 4 years (over existing agreed increases) would deliver further savings against the 2023/24 actual budget of £24 billion (using the lower IFS number in the above bullet point).

Sweetening a bitter pill

The future savings against the 23/24 budget are £22 billion from means testing, less the £7 billion increase for the bottom 70%, plus £24 billion from raising the retirement age, giving a total savings of £39 billion per annum. 70% must wait longer, albeit for a bigger pension, but the lose-lose situation for the top 30% (wait longer for less, or nothing at all) needs to be addressed. I don’t argue this to favour the well-off, but because significant changes need the broadest political support.

This can be done in a way that benefits the overall UK economy and stimulates wealth creation. Ideally, we want to incentivise financial independence for the top 30%.

Here’s how:

- Reduce the ‘additional’ top rate of tax from 45% to 40%. Yes, as proposed by the ill-fated Truss government, but this time supported with £39 billion per annum of identified pension savings to pay for it. In 2022, the Treasury estimated this would cost £6.8 billion over 5 years or approx. £1.4 billion per annum(3).

- Reduce the bottom 20% rate for all taxpayers by 2p to 18%. The same Treasury estimate suggested the cost would be £10.5 billion, which would benefit not just the top 30% but also the low-paid (incl. the children of the top 30%)(8).

- This would send a strong signal to overseas investors that the UK was serious about fiscal consolidation and open for business. It would pump money into the economy and allow.

- For greater savings (which support domestic investment) by the top 30% over their working life. The top 30%, by definition, having the most to gain from a robust economy, would enjoy increased returns on their property and investments.

Together, these two actions could reduce our annual savings from £39 billion to £27 billion.

Execution

The challenge is not the plan. The numbers, the split, the sweeteners, and the timing can all be debated. The challenge is the execution.

- Timing — enough time must be given to allow people to make provisions for the new reality, but this need not take decades (as with the currently proposed, more modest changes). For the purposes of this back-of-the- napkin exercise, I’m suggesting 12 years should be enough to adjust to new options:

- Retire as planned, but with delayed government support (with that support increased/reduced as stated)

- Work longer

- Save more

- Tapering the changes would make the transition easier and less ‘blocky’ (where an individual gets penalised because their birthday is one day before or after a particular cut-off date, or their earnings moved them from one bracket into the next). The more we taper, the more we impact the outcome — I have not estimated for these permutations.

- I’d phase in the tax cuts earlier, thus eating into the £27 billion per annum of savings which are realised in 12 years’ time. The cost of introducing the £12 billion tax cuts in full, 12 years ahead of the savings, would be £144 billion (at FY 23/24 costs), negating the entire savings for the first 5 years (so savings arrive in 17 years, and not 12).

- This is because funded tax cuts 12 years in advance would benefit the economy, provide all taxpayers with the means to save more, and be popular (required for driving through the changes).

In Summary

I’m not under any illusion that the numbers presented here are purely illustrative, rough estimates of what could be achieved. If we don’t take appropriate measures, though, the cost would become increasingly unbearable and more draconian measures would be forced upon us.

Savings can be made in three ways:

- Means testing the top 30%

- A phased raising of the pension age by a further four years, in addition to the two years already agreed

- Linking future pension levels to, not above, GDP growth levels.

The economy benefits in the following ways, with those losing pension entitlements having the most to gain from a thriving economy:

- An annualised saving of £27 billion per annum in 23/24 terms, in this indicative example, realised in full in 17 years’ time.

- An immediate £12 billion per annum tax cut to the higher (£1.5 billion) and lower (£10.5 billion) thresholds.

- Tax cuts either boosting the real economy or investment via savings.

- Strong actions on tackling a thorny political issue would be welcomed by the markets, and together with lower projected debt, should have a positive impact on UK debt interest.

- The lowest 70% of pensioners all get an increase. They are statistically more likely to spend the increase in the real economy ~—-~ a further boost.

- A stronger economy would boost investment returns, whether through shares, property or other. The principal beneficiaries would be the same top 30% sacrificing some or all of their state pension.

( Just) some of the most obvious outstanding questions:

- If this isn’t the way forward — what is? How else can we rethink future pension spending commitments? How can we better support the poorest pensioners whilst reducing the overall burden?

- Are the groups to target even 30%? Why not 10% or 40%? My figures are purely an example. How would this be calculated in a fair, equitable way, reducing the desire to find loopholes?

- How to taper the brackets so an individual is not adversely affected by their birthday or lifetime earnings, thus moving them from one bracket to another?

- How to stagger the increase in pension age to give people time to plan?

- How far into the future would the changes need to be?

- Are the tax cuts the right cuts aimed at the right people (to get their buy-in and benefit the economy)? How could we do it better?

- What’s the equitable thing to do re: private and public pensions?

I’m sure this is just the tip of the iceberg of many hyper-complex questions, but not insurmountable if the political courage and will were there to look at the problem more honestly.

- Institute for Fiscal Studies (2023) ‘How have government revenues changed over time?’ Available at: [https://ifs.org.uk/taxlab/taxlab-key-] questions/how-have-government-revenues-changed-over-time

- Institute for Fiscal Studies (2022) ‘Mini-Budget response.’ Available at:

- Hansard – UK Parliament (2025) ‘Old Age Pensions (Great Britain and Ireland).’ Available at: [https://hansard.parliament.uk/commons/1910)-] 03-10/debates/8129e546-1a85-4700-8b31-369f106fc20d/OldAgePe) nsions%28GreatBritainAndIreland%29)

- Office for National Statistics (2018) ‘Past and projected period and cohort life tables, 2018-based,’ Available at: https://www.ons.gov.uk/ peoplepopulationandcommunity/birthsdeathsandmarriages/lifeexpec tancies/bulletins/pastandprojecteddatafromtheperiodandcohortlifeta bles/1981to2068

- Institute for Fiscal Studies (2024) ‘Pensions: five key decisions for the next government,’ Available at: https://ifs.org.uk/publications/pension s-five-key-decisions-next-government

- RSM UK (2025). The cost of the personal tax cuts,’ Available at: https://w ww.rsmuk.com/insights/weekly-tax-brief/the-cost-of-the-personal-t ax-cuts

- Pensions Archive (2024), The History of Pensions in the UK. Available at: https://pensionsarchive.org.uk/wp-content/uploads/2024/02/The-H istory-of-Pensions-in-the-UK-Website-PDF.pdf

- UK Office for Budget Responsibility (2024). ‘Welfare spending: pen- sioner benefits.’ Available at: [https://obr.uk/forecasts-in-depth/tax-by-] tax-spend-by-spend/welfare-spending-pensioner-benefits/

- Kirk-Wade, Esme (2023). ‘The triple lock: How will State Pensions be uprated in future?’ House of Commons Library. Available at: https://com monslibrary.parliament.uk/the-triple-lock-how-will-state-pensions– be-uprated-in-future/

- GOV.UK, (2023). ‘State Pension Age Review 2023,’ Available at: https://www.gov.uk/government/publications/state-pension-age– review-2023-government-report/state-pension-age-review-2023

- Office for National Statistics (2024). ‘National life tables — life ex- pectancy in England and Wales.’ Available at: https://www.ons.gov.uk/ peoplepopulationandcommunity/birthsdeathsandmarriages/lifeexpec tancies/bulletins/nationallifetablesunitedkingdom/2021to2023

- GOV.UK (2014). ‘The new State Pension.’ Available at: https://www.go v.uk/new-state-pension/what-youll-get