“Aquaculture is the fastest growing food production sector in the world, and is key to feeding a growing population sustainably.”

FAO (Food and Agriculture Organisation of the UN)

“If we are serious about food resilience and climate change, aquaculture must be part of the solution. It produces healthy food with a fraction of the carbon footprint of land-based farming.”

House of Lords debate, 2020

Growth focused on disadvantaged coastal communities

In the last chapter we agreed we want a million+ people off welfare and into work. It means we need a huge number of new jobs, at the right skill level, preferably where those on welfare currently live. Of course, the UK should continue to seek growth in existing areas of strength for the UK — financial and professional services, creative industries, technology and pharmaceuticals. But many of those currently on welfare don’t live in Cambridge or Canary Wharf – many live in coastal towns.

I must admit I never thought I’d be championing the opportunities for the UK to become the seaweed capital of the world, but here goes. Would a sensible person be interested in:

- Revitalising hundreds of coastal towns with the creation of thousands of jobs and significant infrastructure — the very towns we want to give opportunities to escape welfare?

- 0.3-0.5% improvement to GDP and an increase in UK Government receipts of £2-£3.5 billion per annum?

- Improving the nation’s food and energy security, trade deficit, supporting commitments to net-zero, whilst reducing reliance on more expensive options?

- Reduced over-fishing, protection of marine ecosystems, leverage with our European partners?

Some context

Exacerbated by the financial and COVID crises, UK GDP growth over the last 15 years has been sluggish. Q4 2024 UK GDP was just 3.4% ahead of pre-COVID levels, which compares poorly to 4.9% in the Eurozone and 12.2% in the US(1).

Coastal towns fare particularly badly compared to their inland equivalents:

- Employment is down in 50% of coastal towns vs. 37% of non-coastal areas(2)

- Population declined in 32% of coastal communities vs. 16% elsewhere between 2009-18(2)

Many coastal towns are classified as “residential” with high deprivation, limited local employment opportunities and higher reliance on benefits(2). We saw in a previous chapter how we wish to support those on welfare by nudging them back into employment — what we need are the jobs in coastal communities where the claimants live.

Food and energy security is now considered increasingly urgent. In 2023, the UK imported 6-7 million tonnes of food worth approximately £61 billion, leading to a trade deficit in food of approximately £36 billion(3).

What you need to know

- Aqua farming is the cultivation of fish, shellfish, and seaweed. It is widely used in China, Japan, Norway, the US, and South Korea.

- With 2 million dry tonnes, China accounts for around 58% of global seaweed production(4).

- In 2021, the UK farmed 217,000 tonnes of fish and shellfish, valued at £1 billion, a 13% decrease in value compared to 2020(5).

- The Scottish salmon farming industry dominates the industry, accounting for 87% of all UK aquaculture production in 2019. Mussel and oyster farming accounts for some of the rest. Employment in 2019 was estimated at 3,400 people(6).

- Seaweed supports fish farming through ‘ Integrated Multi-Trophic Aqua- culture’ (IMTA), resulting in improved water quality and oxygen produc- tion, more and better habitats and marine food chains. More importantly, it can be harvested for use in food products, pharmaceuticals, biofuel, and is extensively used in other industries like cosmetics .

- Seaweed captures CO2. One hectare captures between 2-8 tonnes of carbon per year, depending on the species, growing conditions and farming methods(7). It does this through photosynthesis, carbon sequestration, and reduces future emissions as a replacement, e.g. it can be used in biodegradable plastics, biofuels, or livestock feed, further reducing emissions.

“Aquaculture, especially when done in innovative and sustainable ways, can be part of the solution to global hunger, climate change, and biodiversity loss.” — Monica Jain (Founder, Fish 2.0)

The Dutch model

The Dutch are the leading European pioneers. Their ‘North Sea Farm 1’ spans 5 hectares and is the first commercial-scale seaweed farm co-located with an offshore wind farm. In its first year, it’s expected to produce at least 6,000 kilograms of fresh seaweed(8).

Dutch researchers have modelled scenarios where up to 790km² might be used for seaweed cultivation in the Dutch North Sea — within a broader national Exclusive Economic Zone of 57,000km². These projections are preliminary and not reflective of committed policy (9).

What to do?

The UK should build on existing UK expertise at a scale unmatched anywhere else in the world. In short, our ambition should be to become an aquafarming superpower. Engineering a new, multi-faceted industry is complex, but here are some thoughts to start the conversation:

- The size of the UK is just under 250,000 sq.km(10). Approximately 70% or 17 million hectares of land is attributed to the broader agriculture industry(11).

- Our (domestic) maritime Exclusive Economic Zone (EEZ) is three times the size of the UK land mass at 773k sq.km — one of the largest in Europe and almost fourteen times the size of the Dutch EEZ(12).

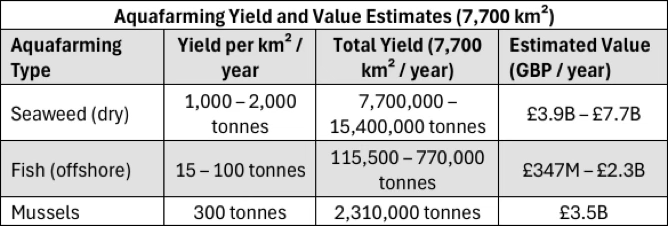

- 1% of our EEZ turned over to aquafarming farming equates to 7,700 sq.km of new ‘farmland’, plus the associated benefits of fishing and shellfish(13).

The Results

Economic Benefits:

- The table below suggests direct returns from fully operational farms range from £8-£14 billion per annum, with an overall benefit to the economy of more than £50 billion. Government finances would benefit from increased tax take and lower spending on welfare.

- This is how the revenue works: In UK waters, estimates suggest 1,000- 2,000 tonnes of dry seaweed can be harvested per sq km per year(14). It means 1% of the UK’s EEZ turned over to farming could generate 7.5-15 million tonnes (4-7 times China’s production)(15).

Market prices per tonne for seaweed vary, depending on use:

- Raw seaweed: $500–$1600 (depending on species and quality)(16)

- Dried seaweed: $1,000–$5,000 (for high-value food products)(17)

- Seaweed-based biofuel: approximately $100–$300(18)

- Seaweed extracts (alginate, carrageenan, agar): $2,000–$10,000

- A conservative median price of $600 per tonne would generate £4.5–9 billion. Even at the very bottom end of our estimates ($150 per tonne), our harvest would generate £1–2 billion.

- Current UK revenue from fishing is £1.1 billion. A 50% increase in the UK catch generates another £550 million, through the creation of 7.7k sq.km of fertile fishing grounds and a further £3.5 billion from shellfish.

Strategic Benefits

What cannot be quantified without deeper research is the positive impact on jobs and local economies in coastal communities.

Across the three food categories in the table above, the UK would secure control in its territorial waters of at least 10 million tonnes of food — enough for 150 kg for every man, woman, and child in the country — not the most varied diet, but a step change in our food security. Till it was needed, it would lower prices and boost food exports/reduce imports.

In a future chapter on energy, we will review the growing importance of biofuels. Till an embattled, isolated Britain makes an emergency shift to a domestic seafood diet, our seaweed crop can power this growing, green energy source — improving our energy security. Indeed, the UK currently provides biofuel subsidies to the leading player (Drax), which could be repurposed to fund pilots of the farms.

Net-zero

UK waters are cooler and nutrient-rich, favouring species like kelp and dulse. Generally, these species absorb CO₂ at the lower to mid-range, closer to 40 tonnes per hectare per year(19). Adjusting for UK conditions, the CO₂ capture per square kilometre (100 ha) could be 400–800 tonnes per year. With 1% of our EEZ turned over to farming, 7,700 sq.km would capture between 3 million and 6.2 million tonnes of CO2, equivalent to 375,000 and 770,000 average UK households, between 1.3% and 2.8% of total UK households. Not huge, but not nothing either.

The Costs

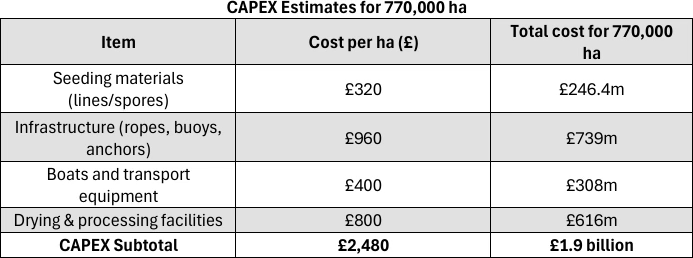

As with all chapters, the numbers here are rough estimates, but my (very) rudimentary research, coupled with an assumption that the Dutch have done their homework, suggests this vision is both affordable and achievable, and someone, somewhere, should have a closer look.

What’s more, we can repurpose existing spend to fund farm pilots. In the chapter on energy, we discuss UK government subsidies to Drax, which runs the Drax power station in Yorkshire. They use these subsidies to import 7 million tonnes of wood pellets from North America, and since 2021 averaged approximately £750 million per annum. It means we could bring forward several years of future subsidies to start setting up our own global leading aquafarming industry.

Other benefits

- Impacted coastal towns would become more vibrant and dynamic, making other investments such as tourism more likely.

- Access could be used in negotiations with our European partners. We will not be ready when the current Transitional Period (2021-26)(20) comes to an end, but our negotiating position will be much enhanced.

- UK would become a world leader not just in aquafarming, but marine biology and research, biofuels and bio-plastics.

- See the separate chapter on international aid (Chapter 7) where we use this leadership to support large-scale projects in the seas off Africa, South America, and Asia. Creating thousands more local jobs, food, and energy in emerging markets, the UK could potentially feed about 50 million people per annum, with the UK shareholding in these projects forming part of a UK Sovereign Aid Fund.

( Just) some of the outstanding questions

- Totally fine if this solution isn’t for you, but if not, what is? How else could we provide jobs and investment in those areas that need it? How else could we significantly impact food security and net-zero?

- Would we be investing so that EU fleets can benefit? Could we list the farms as privately owned, leasing the land to companies so we can better control access?

- Where’s the best place to locate farms a third the size of Wales to benefit the most communities?

- How to transition the UK into eating more fish? The seaweed can wait till geopolitics dictates, or we have no other options.

- Am I going to get into trouble with the Crown Estate?

- GOV.UK (2022). ‘Food statistics in your pocket.’ Available at: https://w ww.gov.uk/government/statistics/food-statistics-pocketbook/food-s tatistics-in-your-pocket

- Global Newswire (2025).’Commercial Seaweed Market Set to Reach Valuation of US$ 16.58 Billion By 2033.’ Available at: https://www.gl obenewswire.com/news-release/2025/02/03/3019423/0/en/Comme rcial-Seaweed-Market-Set-to-Reach-Valuation-of-US-16-58-Billion– By-2033-Astute-Analytica.html

- Marine Management Organisation, (2024). ‘MMO1381: Socio- economic Baseline for the east marine plan areas.’ Available at: https://a ssets.publishing.service.gov.uk/media/67890cf3976cb51ae1573510/ MMO1381_Socio-economic_Baseline_for_the_east_marine_plan_ areas

- LANTRA (2025). ‘Aquaculture — Industry Overview.’ Available at: <https://www.lantra.co.uk/training/aquaculture>

- Anthropocene Magazine (2025). ‘Are seaweed farms ready to issue carbon credits?’ Available at: https://www.anthropocenemagazine.org/2025/ 01/are-seaweed-farms-ready-to-issue-carbon-credits/

- Plymouth Marine Laboratory (2024). ‘World’s first co-located commercial-scale seaweed farm and offshore windfarm announced.’ Available at: https://pml.ac.uk/news/worlds-first-co-located-commer cial-scale-seaweed-farm-and-offshore-windfarm-announced/

- GOV.UK (2023). ‘Agricultural land use in the United Kingdom.’ Available at: [https://www.gov.uk/government/statistics/agricultural-land-use-] in-the-united-kingdom/agricultural-land-use-in-united-kingdom-at– 1-june-2023

- Marine Management Organisation (2019). ‘Identification of areas of aquaculture potential in English waters (MMO 1184).’ Available at: https://assets.publishing.service.gov.uk/media/5dfb8f9840f0b6665e8 01834/MMO1184_AquaPotential_forPub_191210.pdf?m

- Frontiers in Marine Science (2023). ‘Atmospheric CO₂ emissions and ocean acidification from bottom-trawling.’ Available at: [https://www.] frontiersin.org/journals/marine-science/articles/10.3389/fmars.2023. 1125137/full

- Global Newswire (2025). ‘Commercial Seaweed Market Set to Reach Valuation of US$ 16.58 Billion By 2033.’Available at: https://www.gl obenewswire.com/news-release/2025/02/03/3019423/0/en/Comme rcial-Seaweed-Market-Set-to-Reach-Valuation-of-US-16-58-Billion– By-2033-Astute-Analytica.html

- Alaska Fisheries Development Foundation (AFDF) (2022). ‘Estimating Production Cost for Large-Scale Seaweed Farms.’ Available at: https://a fdf.org/research-library/estimating-production-cost-for-large-scale– seaweed-farms- Seaweed Extract Market was Valued at $16.5 Billion in 2023 and is Projected to Grow to $20.9 Billion by 2029.’ Available at: [https://www.] globenewswire.com/news-release/2024/09/24/2951951/0/en/Globa l-Seaweed-Extract-Market-Report-2024-Seaweed-Extract-Market-w as-Valued-at-16-5-Billion-in-2023-and-is-Projected-to-Grow-to-20– 9-Billion-by-2029.html