“High energy prices act as a tax on the entire economy—they depress consumption, raise production costs, and slow growth.”

—Christine Lagarde, former head of the IMF and ECB president

“Energy is the lifeblood of the economy. Without secure and affordable energy, we cannot sustain industry, jobs, or living standards.”

Margaret Thatcher (paraphrased)

We need secure, sustainable, cheaper energy. We can create a step change in our current position, not least by linking up with some of the solutions explored in earlier chapters. As before, the research was rudimentary, but I believe it to be materially correct. Below, we discuss not what should be done, but what could be done to provoke a more mainstream conversation.

Would a reasonable person be interested in:

- Repurposing existing spending commitments to become a global leader in biofuel, taking back 100% control of the raw ingredients, creating thousands of jobs, improving our balance of payments and energy security?

- Fully funded increase in solar power without turning a single field over to solar farms, whilst generating £30 billion return for the Exchequer?

- Getting UK leadership in modular nuclear reactors (finally) off the ground?

- Regaining competitiveness with lower energy bills?

What you need to know

The UK’s energy supply is underpinned by a diverse mix of energy sources, policies, and ongoing infrastructure developments:

- Fossil Fuel Dependency: In 2024, 75% of all energy consumption came from fossil fuels, 2% down from 2023 and the lowest to date(1).

- Renewable sources: The other 25% came from renewable energy generation, which contributed 51% of the UK’s electricity generation in 2024. 30% of this 51% comes from wind power.

- Future Demand: The National Electricity System Operator (ESO) expects peak electricity demand to increase between 26% and 51% in 2035 compared to 2022 levels(2).

- Infrastructure projects build resilience, such as the Xlinks Morocco- UK project, a 3,800 km subsea cable to allow energy imports from ‘Morocco’s renewable energy sources(3).

- Biomass Subsidies: In 2024, UK households contributed £869 million in public subsidies to the Drax biomass power station(4).

- Market-leading technologies: The UK is contending for market leadership across several potentially game-changing energy solutions, including modular nuclear reactors, biofuels, and tidal power.

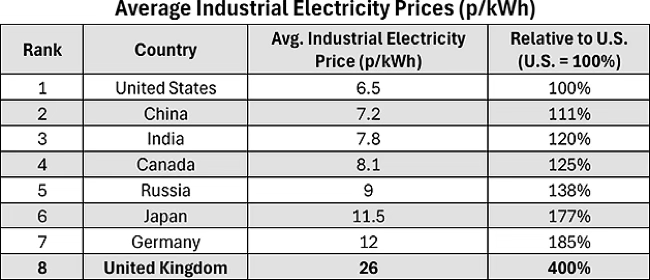

- Expensive energy: Electricity in the UK costs more than 400% than in the US and more than double our continental competitors, impacting industrial competitiveness and spending in the rest of the economy.

What to do?

Bio-mass subsidies

“Modern bioenergy is the overlooked giant of the renewable energy field. It accounts for half of all renewable energy consumption today — as much as hydro, wind, solar and all others combined.”

World Energy Outlook 2018

After wind power, biomass is the second largest contributor to the UK’s renewable energy. One of the largest players is Drax Power Station, which contributes approximately 4% to 5% of the UK’s total electricity supply using imported wood pellets. Its share of the UK’s renewable energy in 2024 was approximately 8%, down from 11% as other sources have grown(5). Drax subsidies vary, but between 2021 and 2024 averaged approximately. £750 million per year, and have been hugely controversial. In short, the wood pellets transported by ship all the way from North America might not be as green as stated.

In another chapter, I talk about regenerating our coastal areas by transform- ing the UK into the global leader in aquafarming. One of the by-products of converting just 1% of our maritime economic zone would be an annual crop of between 7-15 million tonnes of seaweed, one of the principal uses of which is…biofuel.

Drax uses between 6-7 million tonnes of wood pellets per annum. In 2022, 69% of these were imported from the US, 12% from Canada(6). The contract has recently been extended from 2027 to 2031. The pellets subsidy could be reinvested in UK waters. We could take future spending commitments from 2032 and bring them forward to get the farms up and running in time. Any delay could be covered with annual Drax extensions. The site of the first aquafarms could be in the North Sea, 20-100 miles from the power station, rather than the current 4,000 miles travelled by the pellets.

“If sustainably sourced, bioenergy can be a game-changer in the energy transition. It’s the only renewable that can supply all sectors: electricity, heat, and transport.”

Fatih Birol, Executive Director of the IEA

This would be an immediate improvement in our balance of payments. Farming the biomass would create thousands of jobs in coastal communities (for full details, see Chapter 4 on turning the UK into an aquafarming superpower).

Unlike trees, seaweed biomass regenerates in years, not decades, and soaks up more CO2, meaning we could replace some of the more expensive net-zero proposals. Energy security would be improved by being in full control of the raw ingredients.

Biomass world leader

This control and other stated benefits shift the debate on renewable energy. Expanding our farms, we could export any excess fuel (like the US and Canada do today) or invest in further power stations for our domestically produced biomass fuel. This would turn the UK into a global leader in a sector where the market is anticipated to grow from $134 billion in 2023 to $204 billion by 2030 (a compound annual growth rate (CAGR) of 6.3%) (7). In Europe, the market is expected to expand from $58 billion in 2025, with a CAGR of 6.07%.

The UK is currently ranked 4th in the world using 6.7 million tonnes of oil equivalent (Mtoe), ahead of Japan and Italy, approximately half of Germany and Brazil (approximately 12 Mtoe), and a third of the US (approximately 19 Mtoe)(8).

Global leadership would create significant opportunities abroad in two ways.

- Firstly, we could be a leading contender to support any country looking to diversify its renewable energy. Crucially, we would be offering British expertise not just in power generation, but also in sustainable fuel via aquafarming — no other country does this.

- Secondly, I talk in a separate chapter about how the UK could repurpose its international aid budget to deliver a step change in both support for developing countries and ROI for the UK. With joined-up thinking across our newfound expertise (in aquafarming and biofuel), we could feed millions, create thousands of jobs, contribute to net-zero on a global stage, support British expertise in new markets, and supply significant green energy to millions of people currently in poverty.

Solar power

“Innovation in solar is critical. Cheap, reliable, and clean electricity is the foundation of a modern economy.”

Bill Gates

Would a sensible person be interested in a fully funded 40,000 hectares of solar panels that don’t use up a single field?

How we’d do it

Between 2013-2023, the UK built approximately 150,000 new homes annually (9). When we include net additional dwellings, which account for new builds, conversions, changes of use, and demolitions, the average increases to around 207,000 homes per year during the same period(10).

What you need to know

- Solar power’s share of the UK’s electricity generation in 2024 was approximately 5.5% of the UK’s total output, up from 4.8% in 2023.

- During the first quarter of 2025, solar power produced about 4% of the UK’s electricity, with expectations for this figure to exceed 10% during the summer months due to longer daylight hours(11).

- The UK’s total installed solar capacity has been growing steadily, reaching over 14.4 gigawatts (GW) by 2023. This trend is expected to continue. The sources are a mix of rooftop installations and large-scale solar farms.

- Solar farms are highly contentious, causing planning disputes due to their visual impact, ‘Nimbyism,’ and biodiversity concerns.

“The plummeting cost of solar isn’t just a climate win—it’s a massive economic opportunity.”

Michael Liebreich, founder of Bloomberg New Energy Finance

At least three British companies now produce roof tiles that integrate photovoltaic cells directly into the roofing materials. It means they can generate electricity without using any additional space, with reduced concern over the visual impact of standard solar installations. Take-up is slow due to the up-front cost, but they deliver a solid ROI over time:

The numbers

Solar roof tiles are £4-10k more expensive per unit, offset by the ROI: Energy Production & Savings (25 years)

- Average 4 kW solar roof tile system:

- approximately 3,400 kWh/year

- At 30p/kWh, that’s approximately £1,020/year in savings

- Over 25 years: approximately £25,500+ saved

In today’s money, it means each newly built property would generate a net lifetime return of £15k. If the UK made it mandatory for approximately 200k new homes per annum to install solar tiles, over the space of 20 years, the benefits would be:

- 40,000 hectares of solar tiles requiring no additional space or planning

- Generating 6.8 terawatt hours (TWh) per annum or 2.3% of the UK’s total electricity

- Despite the up-front investment, a return over 20 years from the instalment of £3-5 billion. The would be the return for the risk-taker, whether the housebuilder (with government support?) or government borrowing covered by the ringfenced returns

- Once the lifespan of the tiles is exceeded, they would be replaced with cheaper, better tiles, giving a greater return

Further ideas to be explored would include making it mandatory to add batteries. Doing so would increase both energy security and ROI. This is how they work:

- Daytime: Your roof tiles generate electricity — you use what you need.

- Surplus: Extra electricity goes into the battery.

- Nighttime/Cloudy Days: You use stored power instead of buying from the grid.

- When Full: Any excess beyond battery capacity is exported to the grid.

You can also charge the battery from the grid at cheap off-peak rates and use that energy when prices are higher (a.k.a. time-of-use optimisation). Watch this space.

Net-zero and a pragmatic approach to North Sea fossil fuels

“Even in a net-zero world, oil doesn’t disappear overnight. Aviation, shipping, petrochemicals—these sectors will rely on oil for years to come.”

Fatih Birol, Executive Director of the IEA

In 2024, the UK had estimated reserves of 2.3 billion barrels of oil and 1.1 billion barrels of oil equivalent of gas. Current production is expected to halve by 2030 (Energy & Climate Intelligence Unit). We will continue to use fossil fuels for the next decades, albeit at a declining rate. We should maximise extraction of UK reserves where it remains commercially viable to do so, keeping jobs and investment in the UK and supporting the trade balance. This is a decision that could be taken immediately.

Emerging Technologies: Small Modular Nuclear Reactors (SMRs)

“Small modular reactors are a game-changer. They provide reliable, zero-carbon energy, and can be deployed flexibly where it’s needed.”

Bill Gates, founder of TerraPower

With Rolls Royce, the UK is at the forefront of this technology, but whilst backed by numerous governments, no decision has yet been taken. The problem is that they are expensive to both build and run. Each cost approximately £2 billion and powers approximately 1.1 million homes.

What to do?

Partly, this can be solved by scale. What if Rolls Royce were tasked with building a business case not for 2-3 trial reactors in the UK, but for multiple projects over 20+ years? Tens of billions of pounds of investments would be committed based on certain delivery milestones being reached — the price would come down, and private investors would gain confidence.

The funding could come from multiple sources: In previous chapters, we ‘pruned’ approximately £40 billion per annum from the pensions and welfare budgets. Just one year’s savings would pay for 20 such reactors. The biggest challenge at this scale would become the availability of skills rather than cash, and foster a skills boom for young people looking to retrain in a growth industry where the UK should have global ambitions. In other chapters, we explore how to leverage improved access to our universities and fishing grounds through trade agreements and how we

could repurpose the international aid budget to supply sustainable power to developing countries. Both initiatives could include joint partnerships to build SMRs, using British expertise and creating thousands of jobs and skills in the UK and partner countries. Cheaper SMRs would reduce energy prices, putting downward pressure on inflation and make UK goods and services more competitive overseas British investment could be supplemented with partner countries com- mitting some of their own energy infrastructure investment towards this technology, creating a virtuous cycle of downward pressure on costs and British leadership in emerging technologies.

“We’re designing a factory-built nuclear power station that fits on a football pitch and can power a million homes. That’s the scale of the opportunity.”

Rolls-Royce SMR (UK consortium)

( Just) some of the most obvious questions

None of these ideas are new, yet we’re not doing it already. Why not? We’ve already explored how to make significant annual savings in other chapters, so the funding is there. And nothing needs to be invented — biomass power stations, SMR technology, solar tiles — it’s all there. I’m totally fine if these ideas aren’t for you — but let’s discuss the alternatives — we need more, cheaper energy. We want opportunities for British leadership overseas. We want to go green and go big — let’s have that conversation.

- GOV.UK (2025) ‘Energy Trends Jan-Mar 2025.’ Available at: https://ass ets.publishing.service.gov.uk/media/685bda130433072fce0e0fe1/Ene rgy_Trends_June_2025.pdf

- GOV.UK (2023). ‘Statutory Security of Energy Supply Report 2023.’ Available at: https://assets.publishing.service.gov.uk/media/6574ae1a 33b7f2000db72144/statutory-security-supply-report-2023.pdf

- The Times (2025). ‘Plan for subsea cable to send Canada’s clean power to UK.’ Available at: https://www.thetimes.com/uk/environment/article/ plan-for-subsea-cable-to-send-canadas-clean-power-to-uk-npfwt9h mt

- The Times (2025). ‘£10 added to UK energy bills to support wood- burning firm Drax.’ Available at: https://www.thetimes.com/uk/en vironment/article/pay-energy-bills-drax-power-station-885fjsmrp

- Ember Energy (2024). ‘Drax profits rise as electricity generation falls, show new figures.’ Available at: https://ember-energy.org/latest-updat es/drax-profits-rise-as-electricity-generation-falls-show-new-figures

- Biofuelwatch (2023). ‘Drax briefing 2023.’ Available at: https://www.bi ofuelwatch.org.uk/wp-content/uploads/Drax-briefing-2023.pdf

- Grand View Research (2024) ‘Biomass power market size, share & trends analysis report by feedstock, by technology, by region, and segment forecasts, 2024–2030.’ Available at: https://www.grandviewresearch.c om/industry-analysis/biomass-power-market

- Sky News (2024). ‘Government eyes fresh subsidies for controversial burning of wood to create electricity.’ Available at: https://news.sky.c om/story/government-eyes-fresh-subsidies-for-controversial-burnin g-of-wood-to-create-electricity-13050920